Why Agents Avoid the Middle Market, and Who Can Blame Them?

If you’re like most independent or career insurance agents in Canada, your focus is probably on high-net-worth or complex cases. It’s not because you don’t care about everyday Canadian families. It’s because the economics make sense: underwriting a $250,000 term case takes the same time and effort as underwriting a $5 million permanent case, but the compensation is nowhere close.

It’s no surprise, then, that many advisors avoid small and mid-sized term business. But here’s the problem: while agents chase fewer, larger cases, millions of Canadians in the middle market are left underinsured or unprotected altogether.

And that’s not just a social issue. It’s a business opportunity.

The Data: Term Life Is Being Left Behind

According to LIMRA, annualized individual life premiums in Canada grew 5% in the first nine months of 2024. On the surface, that looks healthy. But dig deeper and a different story emerges:

- Whole Life is driving the growth (+9% YTD).

- Policy counts remain flat or even declining, meaning fewer families are actually getting covered.

- Most of the growth is coming from career and affiliated channels, while independents and MGAs are seeing slower results.

Translation for agents: the market is rewarding high-ticket WL sales, but term life, simple, affordable protection for middle-class Canadians, is lagging.

The Market Agents Are Leaving Behind

When the economics reward bigger cases, the middle market gets ignored:

- A $250k term app eats up the same underwriting time as a $5M permanent app.

- Commission structures rarely incentivize small cases.

- Brokers naturally focus on fewer, more profitable placements.

But this gap has created what business strategists call a blue ocean opportunity. While competitors fight over the same pool of wealthy clients, you can build a practice that profitably serves the families the industry forgot.

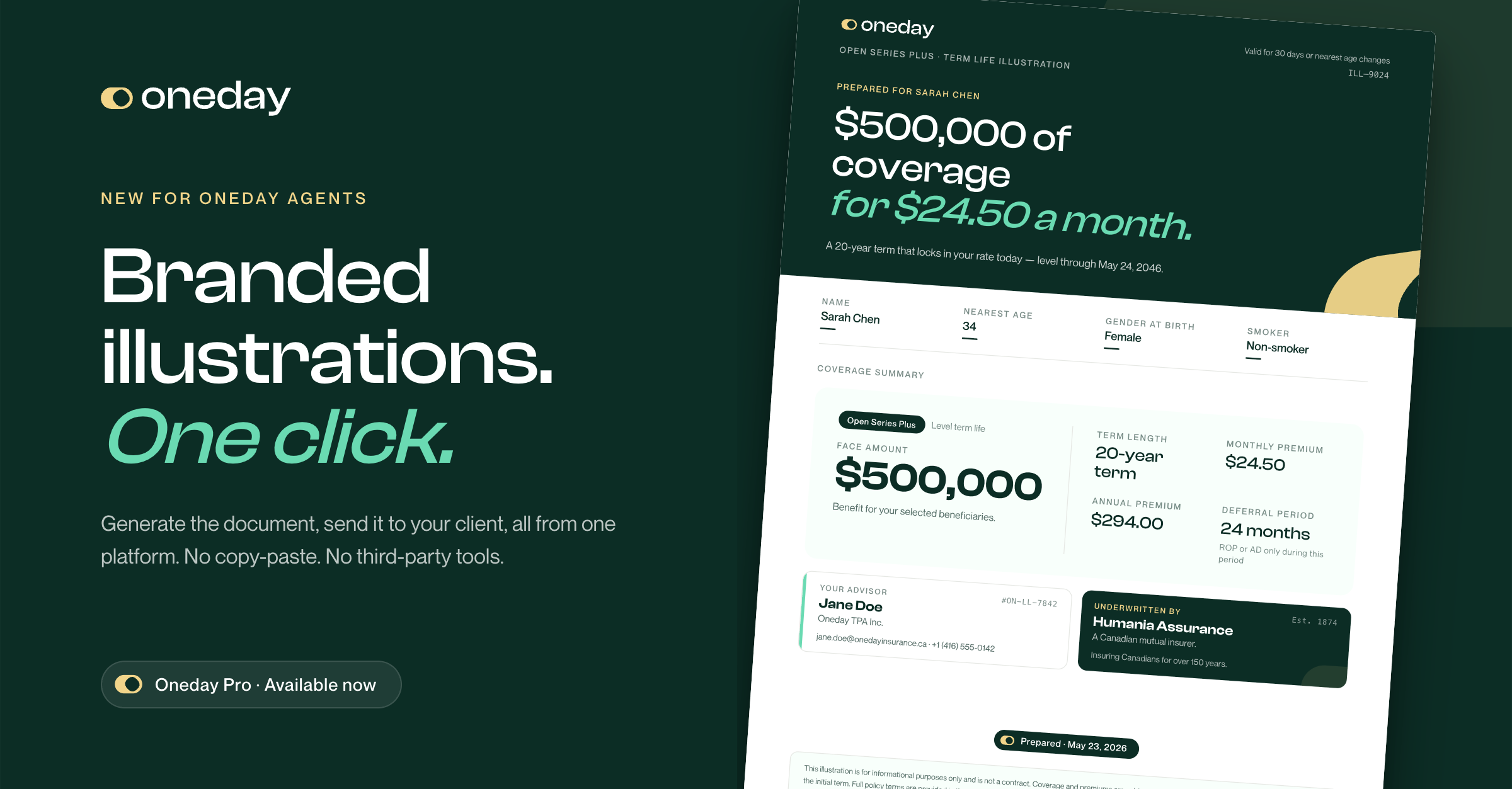

How Oneday Pro Changes the Economics

This is where Oneday Pro comes in. We built our platform to make middle-market term business fast, digital, and profitable.

- Reflexive digital questionnaire: fewer questions, faster completion.

- Digital signature & single-call completion: no back-and-forth paperwork.

- Seamless submission flow: higher placement ratios, less drop-off.

- 24-hour decisions, no medical exams: 83% of applicants qualify for Day 1 coverage.

The result? Agents can write small and mid-sized cases efficiently, at scale, and without sacrificing profitability.

The Human Payoff: More Business, More Impact

Yes, Oneday Pro helps you grow your book and boost efficiency. But it’s also about something bigger:

- Closing the protection gap for Canadian families who need it most.

- Building long-term client relationships that open the door to CI, DI, and other upsells.

- Being known as the advisor who looks after everyday families, not just the wealthy elite.

With Oneday Pro, you don’t have to choose between profitability and purpose. You can have both.

Don’t Ignore Canada’s Biggest Underserved Segment

The Canadian life insurance industry is healthy, but uneven. The wealthy are getting the attention. Everyday families are not. That’s where the real growth is hiding.

Oneday Pro makes serving the middle market not just possible, but profitable.

Ready to capture the opportunity your competitors are ignoring? Learn more about Oneday Pro